Alliance Research

Here, you’ll find some key research from the Alliance and CANNEX, the Protected Retirement Income and Planning Study (PRIP), designed to better understand and forecast retirement income trends; Peak65 – a call to action as the retirement system will be tested like never before in 2024 when we will see the greatest surge of Americans turning 65; and the Alliance and HerMoney that focuses on female financial independence.

PROTECTED RETIREMENT INCOME

AND PLANNING STUDY: Chapter 2

The 2024 Protected Retirement Income and Planning (PRIP) annual study, now in its sixth year, examines the attitudes and behaviors toward retirement savings of Americans ages 61 to 65, known as Peak 65 consumers. PRIP is the only research of its kind that simultaneously surveys both consumers and financial advisors. The second chapter of the report released today highlights critical insights on women entering retirement today.

An alarming 51% of women in the Peak 65® Zone have less than $100,000 in assets, and among single women, this number jumps to 67%. This year, more than 4.1 million Americans will turn 65, entering what the Alliance for Lifetime Income calls the Peak 65 Zone—a historic surge continuing through 2027, highlighting a growing financial crisis among retirement-age women.

The Alliance for Lifetime Income’s 2024 Protected Retirement Income and Planning (PRIP) annual study, now in its sixth year, examines the attitudes and behaviors of Americans ages 61 to 65, known as Peak 65 consumers, toward retirement savings. PRIP uniquely surveys both consumers and financial advisors. The recently released second chapter of the report emphasizes the significant gender divide in the retirement crisis.

“The long-term effects of women earning and saving less are now magnified as millions of Peak 65 women enter retirement,” said Jean Statler, CEO of the Alliance for Lifetime Income. “Women live longer and receive less from Social Security, making them especially vulnerable to outliving their savings. It’s no wonder that this year’s study shows women overwhelmingly prioritize protection in retirement planning. Annuities offer a lifeline by guaranteeing income for life, empowering women to retire with confidence and dignity.”

Key Findings from PRIP Chapter 2:

- 58% of Peak 65 women are married or living with a partner, while 42% are single, divorced, separated, or widowed.

- Single/divorced/widowed women are more vulnerable, with 67% having less than $100,000 in household assets.

- Women are less confident than men about creating their retirement income.

- Women are more likely than men to prioritize “protection” in retirement planning (76% vs. 67%).

- 92% of Peak 65 women working with financial professionals emphasize asset protection, compared to 82% of men.

- 48% of women worry about making complex financial decisions due to potential cognitive decline, compared to 36% of men.

- Only 39% of women understand the role of annuities in retirement planning, compared to 52% of men.

“Women are at high risk of financial insecurity in retirement,” said Jean Chatzky, Education Fellow with the Alliance’s Retirement Income Institute and CEO of HerMoney. “This latest PRIP report shows how much women value protected income—essentially a paycheck for life—that tools like annuities can provide. Unfortunately, there’s a significant knowledge gap preventing women from accessing these tools in time to make a difference.”

ABOUT THE SURVEY

This online survey of consumers was conducted by Artemis Strategy Group from February 15 to March 2, 2024. The 2,516 consumers are ages 45 to 75, of which 505 are an oversample of Peak 65 consumers ages 61 to 65, for a total of 886 Peak 65 consumers.

Data is weighted to align with the population on age, income by gender, race/Hispanic ethnicity, region, work and retirement status, assets, and education.

PROTECTED RETIREMENT INCOME

AND PLANNING STUDY: Chapter 1

The 2024 Protected Retirement Income and Planning (PRIP) annual study, now in its sixth year, examines the attitudes and behaviors toward retirement savings of Americans ages 61 to 65, known as Peak 65 consumers. PRIP is the only research of its kind that simultaneously surveys both consumers and financial advisors. The first chapter of the report released today highlights critical insights on the state of retirement today.

The latest PRIP Study found that half of Americans entering the Peak 65 zone are already retired and claiming Social Security, while more than one quarter of them are financially supporting family members.

Nearly half (49%) of Peak 65 consumers are already receiving Social Security payments. 66% of them have investable household assets of less than $100,000. Among Peak 65 consumers who are now drawing Social Security payments:

- 43% are doing so because of a disability or the inability to work;

- 40% need the income;

- 30% expressed “fear of missing out”, citing concerns that Social Security won’t be there in the future, their payment would be cut, or that they may die before reaching full retirement age.

Financially Supporting Adult Relatives

The ‘sandwich’ generation is growing. Nearly 4 in 10 (38%) of Peak 65 consumers have one or more living parents or in-laws, which underscores the challenge of planning for a long retirement.

Additionally, 28% are currently providing financial assistance to adult relatives, including children aged 18 or older, grandchildren, parents, in-laws and other family members. Of these, 18% of Peak 65 consumers say this financial support cuts into their retirement savings and income.

Challenges in Retirement

Nearly half (48%) of Peak 65 consumers do not think their retirement savings and sources of income will last their lifetime, and nearly a third (31%) worry their retirement income won’t cover their essential monthly expenses throughout their lifetime.

ABOUT THE SURVEY

This online survey of consumers was conducted by Artemis Strategy Group from February 15 to March 2, 2024. The 2,516 consumers are ages 45 to 75, of which 505 are an oversample of Peak 65 consumers ages 61 to 65, for a total of 886 Peak 65 consumers.

Data is weighted to align with the population on age, income by gender, race/Hispanic ethnicity, region, work and retirement status, assets, and education.

PRIP 2024 Chapter 2

To learn more about the findings from the first installment of the Protected Retirement and Income Planning study, visit the links below:

PRIP 2024 Chapter 1

To learn more about the findings from the first installment of the Protected Retirement and Income Planning study, visit the links below:

PRIP 2023 Chapter 1

To learn more about the findings from the first cut of the fourth installment of the Protected Retirement and Income Planning study, visit the links below:

PRIP 2023 Chapter 2

To learn more about the findings from the second cut of the fourth installment of the Protected Retirement and Income Planning study, visit the links below:

PRIP 2023 Chapter 3

To learn more about the findings from the third cut of the fourth installment of the Protected Retirement and Income Planning study, visit the links below:

PRIP 2023 Chapter 4

To learn more about the findings from the fourth cut of the fourth installment of the Protected Retirement and Income Planning study, visit the links below:

PRIP 2022 chapter 1

To learn more about the findings from the third installment of the Protected Retirement and Income Planning study, visit the links below:

PRIP 2022 Chapter 2

To learn more about the findings from the second cut of the third installment of the Protected Retirement and Income Planning study, visit the links below:

PRIP 2021 Chapter 1

To learn more about the findings from the first installment of the Protected Retirement and Income Planning study, visit the links below:

PRIP 2021 chapter 2

To learn more about the findings from the second installment of the Protected Retirement and Income Planning study, visit the links below:

THE STATE OF WOMEN 2022

In partnership with HerMoney, a digital media company, founded by personal finance expert Jean Chatzky, focused on improving the relationships women have with money, the Alliance released The State of Women 2022 study, that focuses on female financial independence.

After years of making progress on closing gaps, climbing ladders and shattering ceilings, we’re learning (and hearing) how the pandemic has set women back. That’s why the Alliance and HerMoney went straight to the source.

The State of Women 2022 study, launched in March 2022, is an ongoing series of surveys of the HerMoney community.

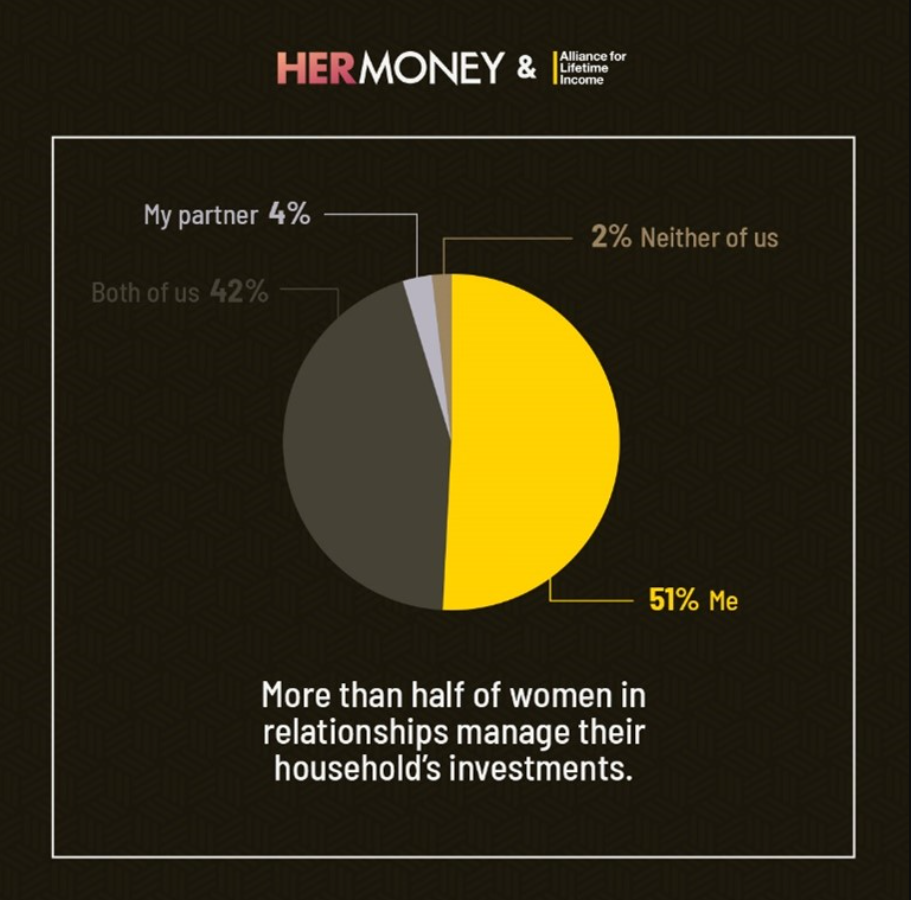

Chapter 1

Women are taking control of their finances, investments and retirement planning

April 12th, 2022

To learn more about the findings from chapter 1, visit the links below:

Chapter 2

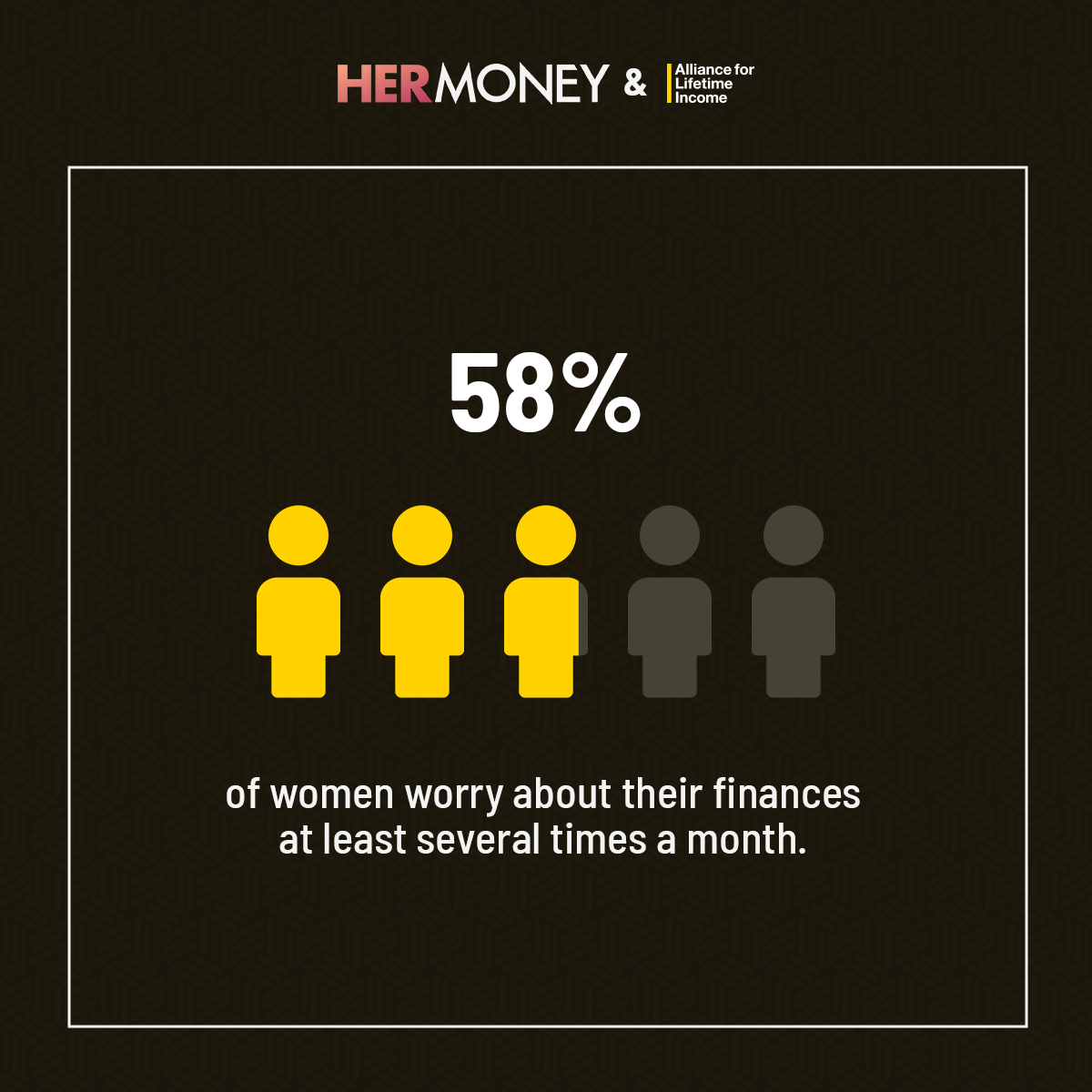

Nearly 3 out of 5 of women worry about money several times a month or more

April 28th, 2022

To learn more about the findings from Chapter 2, visit the links below:

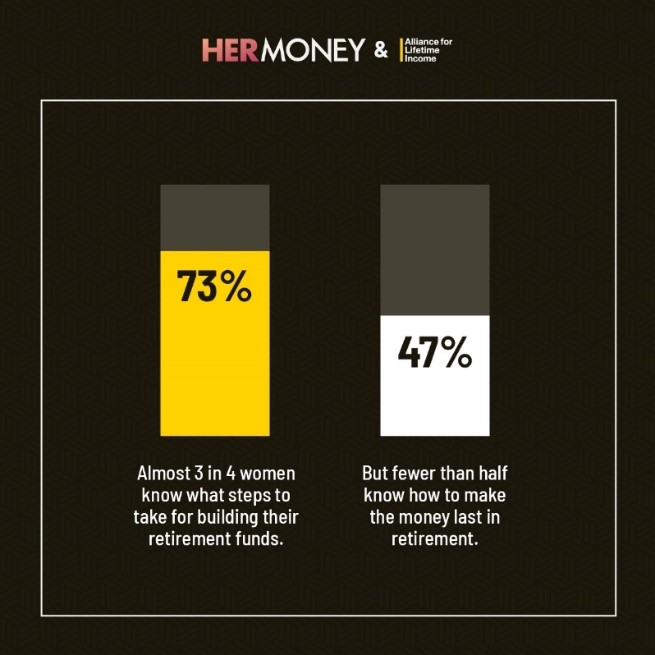

Chapter 3

Less than half of women know how to make their money last in retirement

May 18th, 2022

To learn more about the findings from Chapter 3, visit the links below:

Chapter 4

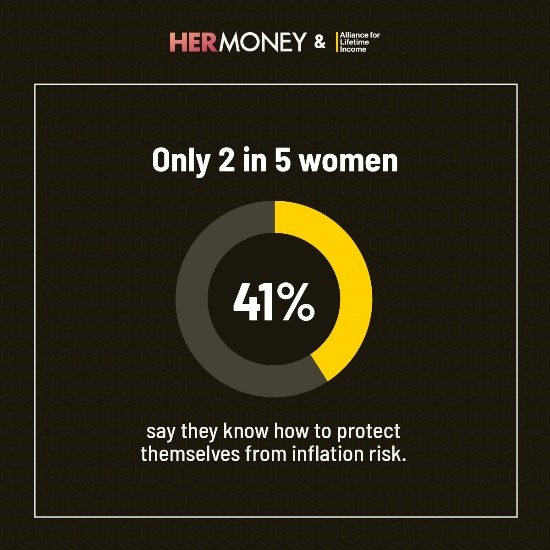

Inflation Risk is the Top Financial Concern for Nearly Three in Four Women

August 3rd, 2022

To learn more about the findings from Chapter 4, visit the links below:

Chapter 5

Two-Thirds of women see a U.S. Recession Ahead, But Plan to double down on retirement savings

November 14th, 2022

To learn more about the findings from Chapter 5, visit the links below:

Peak 65

Peak 65™

Let’s Meet the Challenge of America’s Historic Peak 65 Moment With A New Approach to Retirement Security

The greatest surge of new retirees in the nation’s history is fast approaching. In a mere two years, the US will have more 65-year-olds than ever before. With more than 10,000 people turning 65 every day, it’s a number that will increase to more than 12,000 a day until the nation reaches its Peak 65™ moment in 2024.1 Our nation’s retirement system will be tested like never before.

To meet this challenge, we have issued a collective call to action—based on research—to those with important roles to play in providing retirement security for Americans, including employers, public policymakers and financial professionals.