The “Retirement Answer Man’s” Roadmap to a Confident Future

6 minute read time.

You’ll never be exonerated from three things: Pain, uncertainty, or the need to do work.

If Roger Whitney—better known as the “Retirement Answer Man”—were to get a tattoo, those are the words he’d choose. This philosophy, popularized by psychiatrist Phil Stutz, resonates deeply with Whitney. He believes it applies not just to life, but to retirement as well. “There’s no ‘easy’ button,” he says.

In addition to hosting the Retirement Answer Man podcast, Whitney leads the Rock Retirement Club, where he helps over a thousand individuals approaching or navigating retirement make the most of life’s next chapter.

After decades of fielding retirement questions and helping people chart their personal paths, Whitney has identified key principles that he says can help anyone “rock” their retirement with clarity and confidence.

FOCUS ON PROCESS OVER PANIC

When people reach out to Whitney today, the big question on their minds is: “What the hell is going on?” With markets in flux and economic uncertainty lingering, Whitney says, “We’re driving in fog at the moment and people are heightened and worried.”

So, how do you drive in fog? For Whitney, it’s all about prioritizing “process over panic.” He encourages focusing on what you can control—your “controllables”—rather than reacting emotionally to what you can’t. For example, cutting back on spending or beefing up your emergency fund.

Roger Whitney, The Retirement Answer Man

KNOW THE FINANCIAL PILLARS OF SUCCESSFUL RETIREMENT

Drawing on his over 25 years of experience as a financial professional, Whitney identifies four financial pillars that support a successful retirement:

Vision: With countless possibilities available in retirement, clarity is essential. Whitney suggests starting by identifying your top 10 personal values. These could range from adventure to family—anything that reflects what matters most to you.

Feasibility: Once you’ve defined your values, explore what each one means in practical terms. “You can take a value, flesh out what it means to you, and then you can create a goal,” says Whitney. After setting these goals, assess your resources to determine whether they’re realistically achievable.

Resilience: Retirement plans need to be flexible. “Make the plan resilient enough so you can have optionality,” Whitney says, stressing that life’s unpredictability requires a financial strategy that can evolve. He also challenges the conventional wisdom of the 4% rule.“People’s lives are lumpy. If you follow that construct, you’ll likely end up with a ton of money at the end,” he says.

Optimization: To truly optimize your retirement finances, Whitney recommends pre-funding at least the first five years of retirement with a clear cash flow plan. He then suggests considering permanent income options—like annuities—on the back end of that plan.

TAKE STEPS TO GAIN FINANCIAL CLARITY

Whitney emphasizes that having a structured plan for the next five years is a powerful way to reduce stress and gain financial clarity. “Basically, build a payroll reserve that’s managing sequence of return, but it’s managing the psychological aspect even more,” he explains.

He also recommends maintaining an “upside portfolio” to combat inflation, and—depending on individual needs—considering strategies like buying a personal pension. While not everyone needs every component, having the right mix can provide peace of mind.

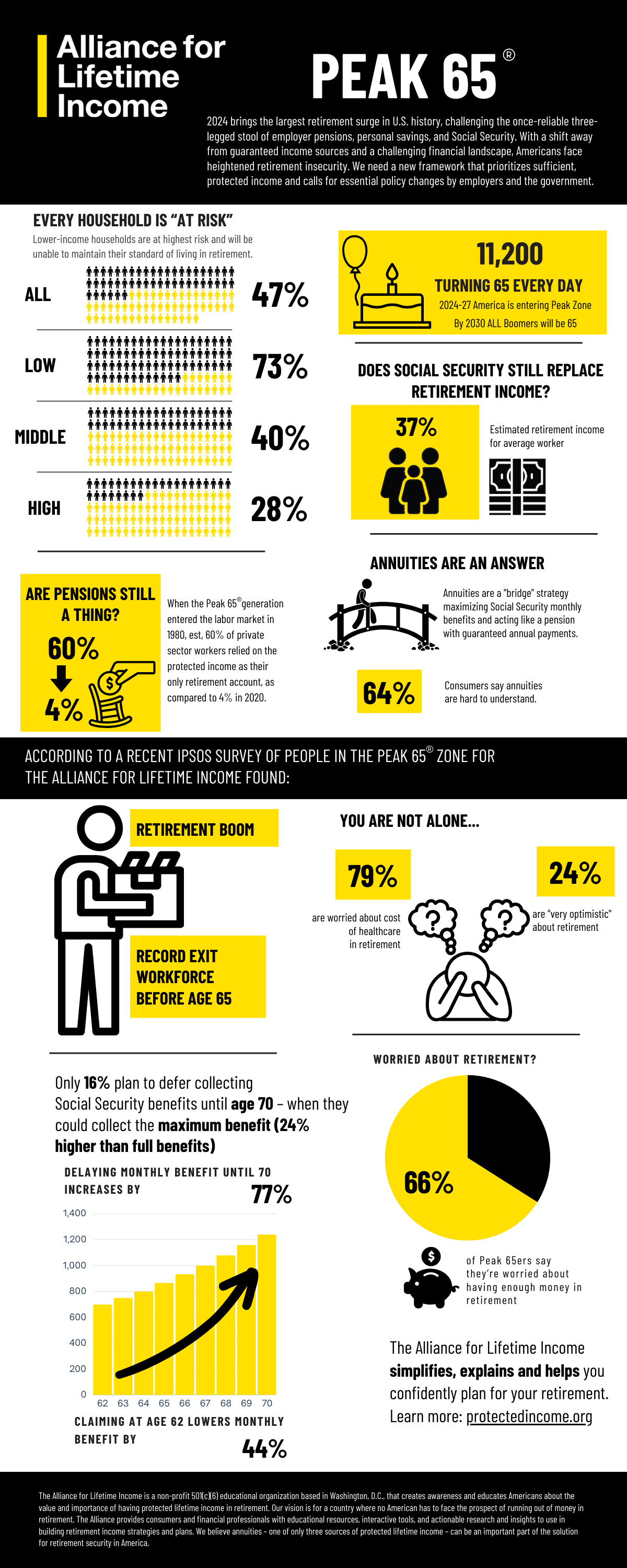

Over the years, Whitney has observed two types of retirement crises: those without enough money, and those who do have enough, but still struggle with a fear of running out. “What that ends up doing is minimizing their life, but also causing them, or the resources, to not do good things, not just for their family, but for the world,” he says. Alliance for Lifetime Income research backs this up, as a recent survey shows 66% of Peak 65’ers are worried they won’t have enough money in retirement.

{kind=link}

RETIREMENT = A PLAYGROUND, NOT A PARK BENCH

“When I started, most retirees were on the park bench of life, and now, more retirees look at it as their chance to get on the playground,” says Whitney.

However, the road to that playground is more complex today. With pensions becoming increasingly rare, many are navigating this phase without a clear roadmap. “Everybody is driving separately, they don’t know who to trust or what to do,” he adds.

Whitney urges retirees to move away from a “trust me” mentality that relies entirely on experts. Instead, he encourages active participation. “You need to participate,” he says. “Trust comes from clarity, efficacy, and agency.”

Related Content:

- Even when they can easily afford it, many retirees are reluctant to spend their savings to enhance their lifestyle. Learn why, here.

- Millions of Americans will retire without knowing whether they will have enough money to cover their expenses. But you can. See if you’re on track by calculating your Retirement Income Security Evaluation (RISE) Score.

- What type of investor are you – an Optimistic Dreamer, Cautious Preparer, Hopeful Striver, Purposeful Planner, or Ambitious Risk-Taker? Find out here.