Analysis: Peak 65 Boom

Date: 08/2/2024

View article on King’s College London

Peak 65’ is the term given to the biggest increase of people over 65 years old the world has ever seen. The UK is not alone where the economic realities of this trends are starting to bite with pressure on Local Authority funding and personal savings to cover retirement and care.

Unlike older retired Baby Boomers, the majority of Peak 65’ers don’t have pensions, which used to help fill that gap left by Social Security. Our current retirement system is obsolete and it’s time for a new retirement security framework.

– Jason Fichtner, Executive Director, Ali Retirement Income Institute, USA

Near-retirees simply aren’t prepared. In the US about half of women between ages 55 and 66 have no retirement savings, compared to 46% of men, according to a 2022 US Census Bureau Survey.

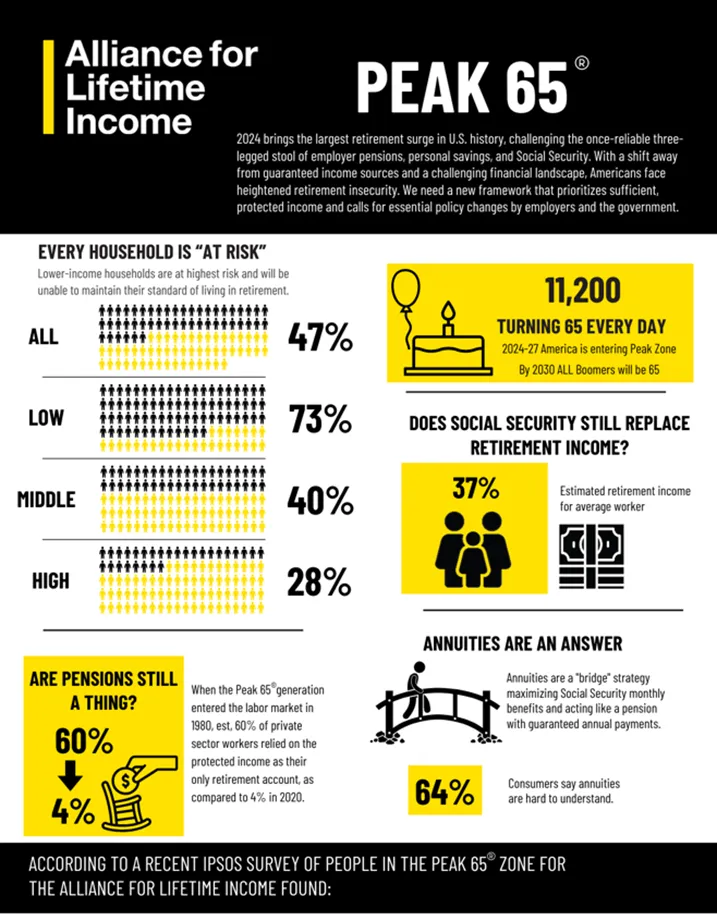

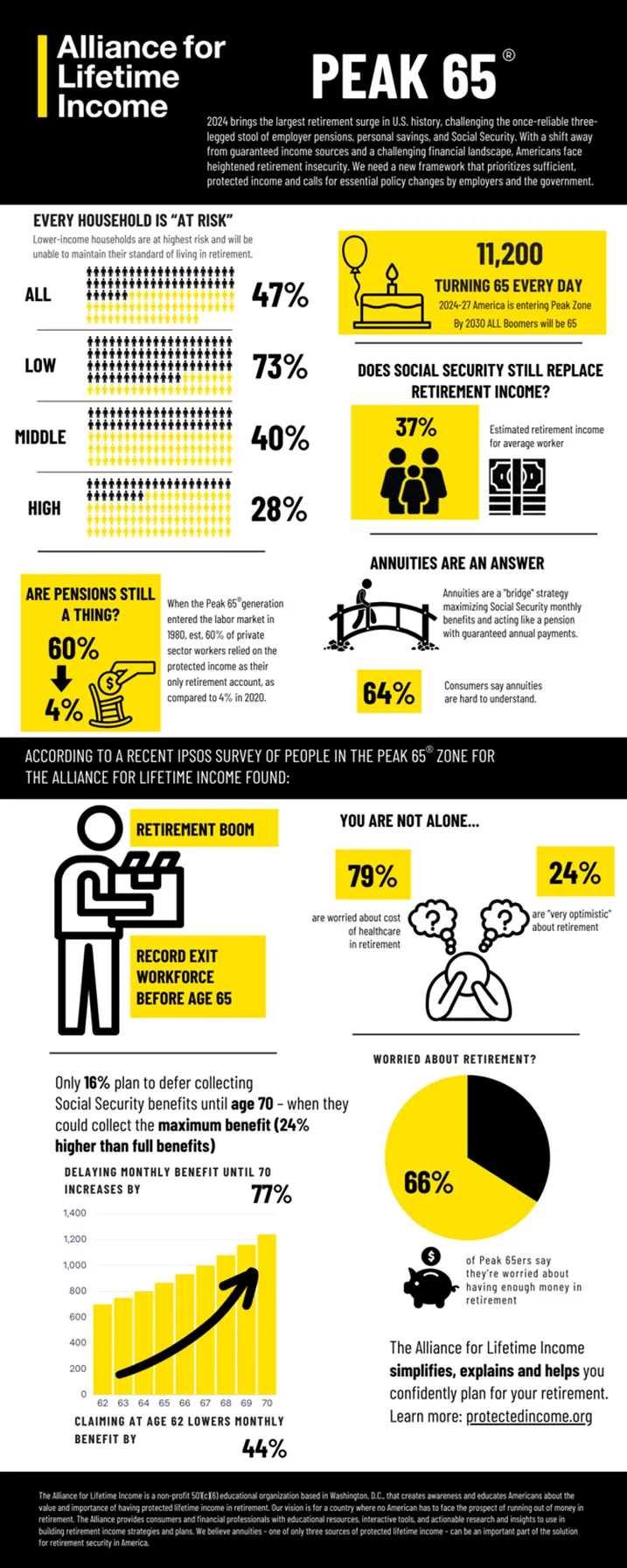

More than 4.1 million people are expected to retire this year, and that figure will continue on through 2027, according to the Alliance for Lifetime Income’s Retirement Income Institute, which has been tracking the “Peak 65 zone.”

This year will bring the largest number of Americans celebrating their 65th birthdays. Although there is no one set age for retirement in the U.S., the age 65 has historically been considered the norm (and for many Americans is their full retirement age for Social Security-claiming purposes).

Near-retirees simply aren’t prepared

About half of women between ages 55 and 66 have no retirement savings, compared to 46% of men, according to a U.S. Census Bureau survey in 2022. The trust funds behind Social Security are expected to run out of money in the next 10 years, at which point beneficiaries could see a 20% benefit cut.

The number of 65-year-olds may be peaking, but we are far from peaking in the challenges of financial insecurity

Having more people living longer can be seen as a positive, and is a nod to scientific advancements — but when it comes to retirement readiness…

we have stormy weather ahead.

– Paul Irving, senior adviser at the Centre for the Future of Aging at the Milken Institute

There are some aspects of society that directly touch older Americans and will be pressured by this demographic bubble. One example is Social Security, which acts as a major source of income for retirees in the U.S. but is currently facing insolvency.

This grim forecast does not take into account a significant influx in retirees beginning to claim benefits in this or the coming years.

Legislative issues aside, the program was not meant to sustain most of Americans’ financial needs — although for many retirees, it is their sole source of income. “Social Security is inadequate to fund the longer lives people are likely to have,” Irving said.

Healthcare is a significant expense for Americans, especially those who are older. Although people may be living longer, they could be faced with the need to manage chronic conditions or plan for long-term care. The need for long-term care will trickle down to younger generations, such as relatives who may have to become caretakers for their aging loved ones.

The Peak 65 Zone is here

The year 2024 marks the beginning of the “Peak 65® Zone,” the largest surge of retirement age Americans turning 65 in US history. Over 4.1 million Americans will turn 65 each year through 2027, which is more than 11,200 every day. Unfortunately, the country’s public and private sector retirement systems have become obsolete, as has the now-antiquated retirement planning approach of focusing solely on accumulating a lump sum of savings rather than the actual income people will need for a retirement that could last 20, 30 or more years. The old metaphor of the three-legged stool of retirement planning—employer pensions, personal savings, and Social Security—no longer holds.

Many households face an uncertain financial future in retirement, with one measure suggesting that about half of all households are “at risk” of not having sufficient resources to maintain their standard of living in retirement.

Retirees face a challenge of having enough income in retirement. And the nation’s retirees face a growing gap in the level of protected income they need and can count on throughout retirement. One research paper estimates that for households with insufficient income in retirement, the gap amounts to an annual shortfall of $7,050. That would amount to an annual national retirement income gap of approximately $230 billion in 2040. Several economic and demographic factors have contributed to this problem.

First, very few private-sector employers still offer a traditional defined-pension retirement plan providing protected income that is guaranteed throughout retirement. This means more Americans are entering retirement with Social Security as their only means of protected income, leaving many exposed to financial insecurity.

Second, since the number of people retiring without a traditional pension has declined significantly over the past several decades, most people are now saving for retirement in defined-contribution plans. This has shifted the nature of protected income in retirement toward receiving pension pay-outs as income in retirement to the need to replace that pension income with protected income solutions generated from defined-contribution plan assets.

As more people enter retirement without a pension, the risk and burden of funding adequate income has shifted entirely to the individual, and many are unprepared to deal with the vast amount of information necessary to make optimal financial retirement income decisions.

Third, a volatile investment market makes it challenging for retirees to generate sufficient and consistent risk-free new income from their retirement savings that keeps pace with inflation and equally important, can last throughout retirement. In recent years, a persistent low-interest rate environment made it difficult for retirees to generate sufficient, if any, income from financial products like certificates of deposit and money market funds.

While interest rates are much more favourable today,10 uncertainty over whether higher interest rates will persist or fall adds further complexity and risk to the retirement income challenge facing retirees. Further, relying on equities and bonds as a primary option for meaningful income generation on savings creates higher levels of ongoing risk for retirement income management, including exposure to sequence of return risk, where negative investment returns early in retirement cannot be overcome.

Fourth, a significant percentage of people are claiming Social Security benefits early and missing out on the larger monthly benefits they could receive if they delayed claiming for just a few more years, depriving them of a much more robust, fully protected income stream throughout their retirement. As a result of these changes in the US retirement system, many Americans lack sufficient, reliable protected retirement income that will last for the rest of their lives, while their life expectancy has increased in recent decades.

It’s time for a new retirement security framework that focuses on the need for sufficient protected income in retirement. This will require fundamental policy changes by employers, the broader private sector, and government. Fortunately, bipartisan support led to the passage of both the Setting Every Community Up for Retirement Enhancement Act of 2019 and the Securing a Strong Retirement Act of 2022 both which greatly improved the environment for creating a new security framework focusing on the importance of protected income in retirement.

The Secure Act provided a provision that made it easier for a retirement plan sponsor to offer an annuity option in a defined-contribution plan. This helps employers to offer an annuity option, traditionally associated with defined-benefit pensions, within a defined-contribution retirement plan.

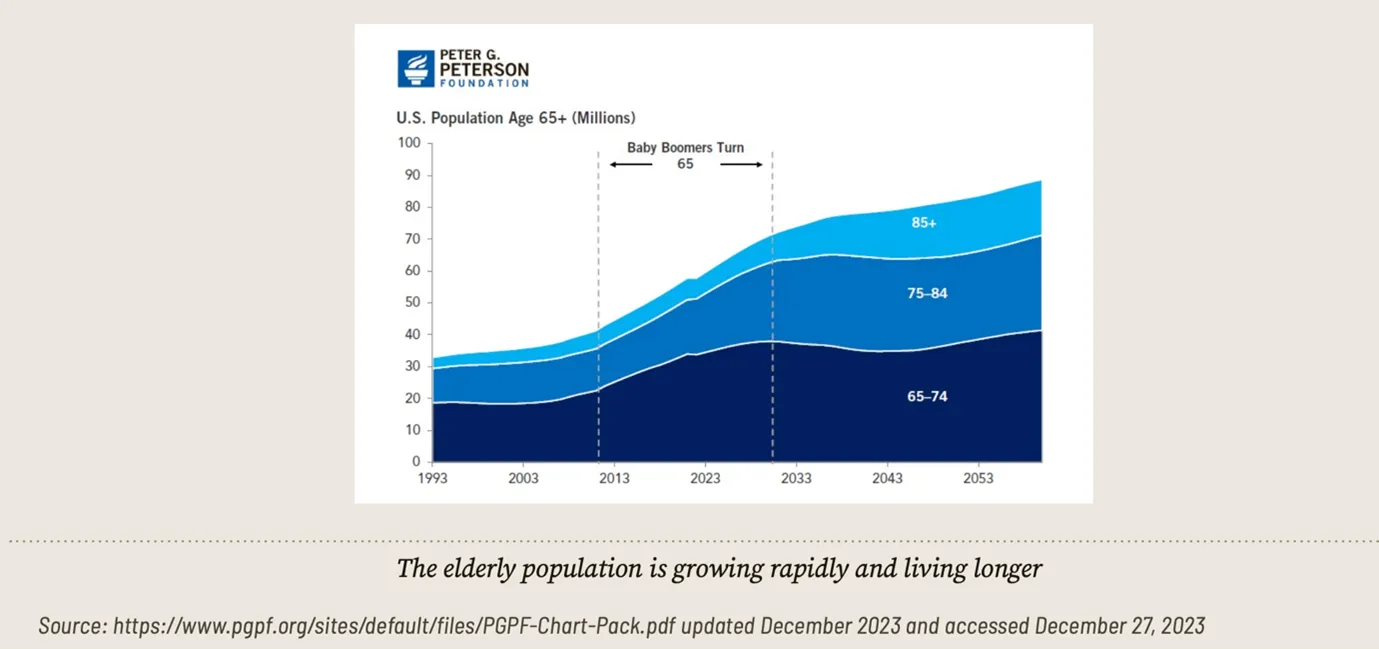

Secure 2.0 increased the amount that individuals can move into a qualified longevity annuity contract (QLAC). The baby boom generation consists of people born after World War II, from 1946 to 1964. There are currently an estimated 72 million people in the boomer generation based on the 2020 U.S. Census, a decline from an estimated 77 million from 2010.

The tail-end of the boomer generation can be called the Peak 65 generation, because beginning in 2024 an average of over 4.1 million people will turn 65 each year through 2027, which is more than 11,200 every day.

By the year 2030, all baby boomers will be age 65 or older.19 Additionally, by the end of the decade the estimated number of people age 65 or older (71 million) will be larger than the number of estimated people under the age of 18 (68 million).

The ratio of beneficiaries to workers has important consequences and implications for the financing of major retirement programs, such as Social Security. As the ratio of people relying on benefits increases relative to the number of workers, the cost of the program as a share of taxable payroll increases.

Beginning in 2024, the nation enters its Peak 65 Zone, where the number of people turning age 65 averages over 11,200 per day through 2027, up from an average 10,000 per day over the previous decade.

By the year 2030, all those of the boomer generation will have reached at least age 65. That year, approximately one-fifth of the US population will have reached age 65, the traditional age associated with retirement. In addition, 2024 marks a historic reversal, when there will be more Americans 65 or over than children under age 15.

These demographic changes will have major implications for the country’s fiscal finances, as well as the retirement security for Boomers and generations that follow. When people in the Peak 65 generation entered the labour market in 1980, approximately 60% of private sector workers relied on the protected income offered through a pension plan as their only retirement account, as compared to 4% in 2020.

According to data released in 2023 by the U.S. Bureau of Labour Statistics, only 19% of all workers participate in a pension plan.

Breaking out the data based on access, 10% of civilian non-union workers had access to a defined-benefit pension, while 66% of private sector union employees had access to a pension. Though a smaller part of the overall labour force, pensions are still popular with private sector union employees and also with workers employed in federal, state and local governments.

Based on the number of active participants in a retirement plan, the number of participants in defined-benefit is dwarfed by those in defined-contribution plans, with 31.9 million defined-benefit participants, including 12 million private sector participants, out of 142.3 million total participants (defined-contribution and defined-benefit private sector plans).

Further, based on data from the Federal Reserve, for those non-retirees with some form of retirement savings, 54% reporting saving in a defined-contribution plan, while only 20% reported having a defined-benefit pension.31 Social Security is still by far the most frequent source of income for those age 65 or older, with 92% reporting receiving Social Security benefits.