Expert Viewpoint: Annuity Education Must Take Center Stage For Advisors to Meet The Demand For Protection in Retirement

2 minute read

A short essay providing a unique perspective on the 2021 Protected Retirement Income and Planning Study

By Michael Finke, PhD, fellow at the Alliance for Lifetime Income’s Retirement Income Institute, and professor and Frank M. Engle chair of economic security research at The American College of Financial Services

By Michael Finke, PhD, fellow at the Alliance for Lifetime Income’s Retirement Income Institute, and professor and Frank M. Engle chair of economic security research at The American College of Financial Services

Americans want the lifetime income security that only annuities can provide. Ninety-one percent (91%) of investors in the 2021 Protected Retirement Income and Planning Study rate protected retirement income as very or moderately important, and 95% feel that it is somewhat or extremely valuable to have guaranteed lifetime income to supplement Social Security income. The ability to provide an income stream that lasts a lifetime is far more important to consumers than other characteristics that financial advisors often value the most, such as asset optimization. A lifetime income stream is the most important attribute of protected income among respondents of all ages, incomes, education levels, and race. Clearly, Americans want the reliability and security of lifetime income.

Americans want the lifetime income security that only annuities can provide. Ninety-one percent (91%) of investors in the 2021 Protected Retirement Income and Planning Study rate protected retirement income as very or moderately important, and 95% feel that it is somewhat or extremely valuable to have guaranteed lifetime income to supplement Social Security income. The ability to provide an income stream that lasts a lifetime is far more important to consumers than other characteristics that financial advisors often value the most, such as asset optimization. A lifetime income stream is the most important attribute of protected income among respondents of all ages, incomes, education levels, and race. Clearly, Americans want the reliability and security of lifetime income.

But the study also reveals a disconnect between what people want and what people know about annuities. Fewer than half (46%) of investors associate annuities with creating a lifetime income stream. The inability to correctly associate annuities with one of their key benefits was even more pronounced among middle-aged (39%) than among retirement-age (49%) investors, and among those with lower levels of education. Women, those with fewer years of education, and lower-income respondents were also less likely to know much about annuities. Only 17% indicate that they are extremely familiar with annuities. Paradoxically, those who placed the highest value on lifetime income are often the groups who say they know the least about the product.

It is not surprising that, despite placing a high value on protected lifetime income, only 1 in 7 investors indicate that they are extremely interested in buying an annuity. They simply do not know enough about the product. The top reasons listed for not buying an annuity include the perception that they can get a better return on other investments, high fees, and lack of awareness.

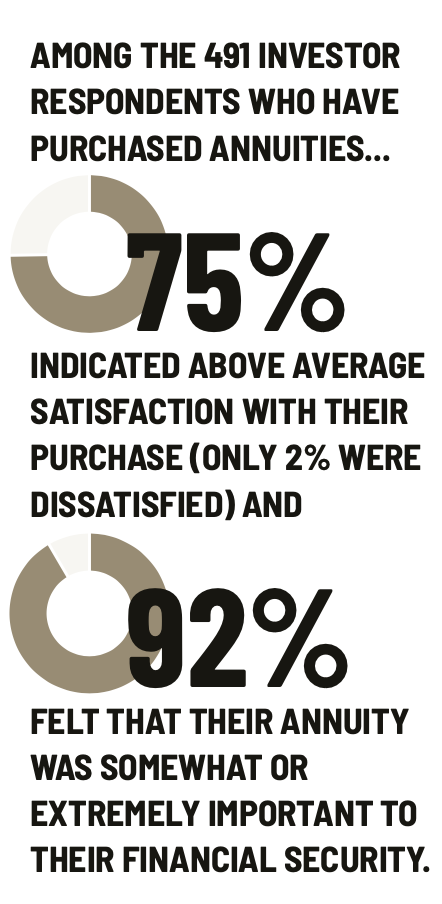

Among the 491 investor respondents who have purchased annuities, 75% indicated above average satisfaction with their purchase (only 2% were dissatisfied) and 92% felt that their annuity was somewhat or extremely important to their financial security.

Financial advisors can bridge this knowledge gap by providing objective information about the benefits and costs of various annuity products. Among the respondents who work with a financial advisor, more than half (57%) say their advisors has discussed annuities with them. There are also clear differences between advisor channels when it comes to the perceived importance of creating a lifetime income stream. While only 40% of Registered Investment Advisers (RIAs) use a retirement income approach developed to provide a lifetime income stream, between 51% and 62% of advisors in other distribution channels employ this approach. The differences are even more dramatic when advisors are asked about the importance of asset protection. While only 58% of RIAs feel that protection is very important, between 78% and 92% of the other five advisor channels included in the study consider protection a very important aspect of retirement planning.

It is not necessarily surprising that investors value what high-quality annuities can provide in retirement. Advisors and the industry can do more to help investors both understand the value annuities provide and navigate complex products to select the right solution which provides the protection investors demand.